Non-Qualified Stock Options, or NQSOs, are a popular form of equity compensation that many companies offer to their employees. Over the years, our team has had multiple clients come to us with questions about how they work, how they’re taxed, and, most importantly, how they can best be managed. So, I thought I’d share some insights on the topic to help you understand how NQSOs might fit into your broader financial plan.

Let’s start with how NQSOs work. Simply put, they give you the right to buy company stock at a predetermined price, known as the “exercise” or “strike” price. This price is usually set when the options are granted and is typically based on the stock’s market value at that time. The idea here is that if your company’s stock price goes up, your NQSOs can become quite valuable.

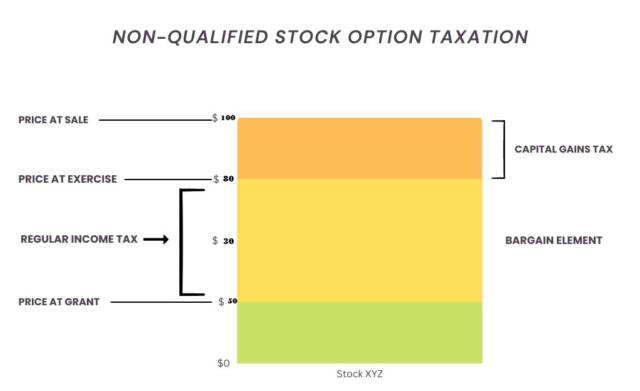

For example, let’s say you’ve been granted NQSOs that give you the right to purchase 1,000 shares of your company’s stock at $50 per share. If, over time, the stock price increases to $80 per share, you can exercise your options and immediately benefit from the $30 per share difference, assuming you sell right away.

However, NQSOs come with some important considerations, especially when it comes to taxation. Unlike Incentive Stock Options (ISOs), which have more favorable tax treatment, NQSOs are taxed as ordinary income when you exercise them. Specifically, the difference between the exercise price and the market value at the time you exercise is considered earned income and taxed accordingly.

For example, if you exercise your right to buy 1,000 shares at $50 each, and the stock is worth $80 per share at that time, you’re essentially earning $30,000 in additional income. Your employer will typically withhold 22% for federal taxes, but depending on your tax bracket, you might owe more. On top of that, you’ll have Social Security and Medicare taxes to consider.

Once you’ve exercised your options and own the shares, the next decision is when to sell them. If you sell the shares immediately after exercising, you won’t owe any additional tax. But if you hold the shares, any increase in value after the exercise date will be taxed as a capital gain when you sell. If you hold the shares for over a year after exercising, the gain will qualify for long-term capital gains tax, which is generally lower than ordinary income tax rates. If you sell the shares within a year, though, the gains will be taxed at the higher short-term capital gains rate.

One of my clients, Sarah (alias), had a great opportunity to exercise her NQSOs a few years ago. She was granted options to buy 1,500 shares of her company’s stock at $60 per share. Over time, the stock price grew to $100 per share, giving her a substantial gain. When her options vested, we discussed the various strategies available to her. Since she didn’t need the money immediately and was confident in the company’s future, Sarah decided to exercise her options but hold the stock for over a year. By doing so, she could take advantage of the lower long-term capital gains tax rate on the $40 gain per share.

Another client, Tom (alias), was in a different position. He was more concerned about market risk and had already seen a lot of volatility in his company’s stock. When his options vested, the stock was trading at $75, with an exercise price of $50. Rather than hold the stock and risk a potential price drop, we decided to do a “cashless exercise,” where he exercised his options and immediately sold the shares. This strategy allowed Tom to lock in his gain and avoid any market downside. He ended up paying ordinary income tax on the $25 per share difference, but he was able to diversify his portfolio right away and reduce his exposure to his company’s stock.

The decision of whether to hold or sell after exercising depends largely on your individual financial situation, tax strategy, and risk tolerance. Some clients prefer to hold onto the stock, hoping for future gains, while others feel more comfortable selling immediately to avoid market fluctuations. It’s important to have a strategy in place before you exercise, especially since the tax hit can be significant.

Ultimately, NQSOs are a powerful tool for building wealth, but they come with complexities that require careful planning. My advice is to think about your long-term goals and make sure your strategy aligns with those. Tax considerations, market risk, and your overall portfolio should all factor into your decision. And as always, our team is here to help guide you through the process and find the best approach for your situation.

Have another form of equity compensation like Restricted Stock Units? Read a previous blog post here – Vesting In Your Future.